By Anton Crabbe 28th May 2025

Intro:

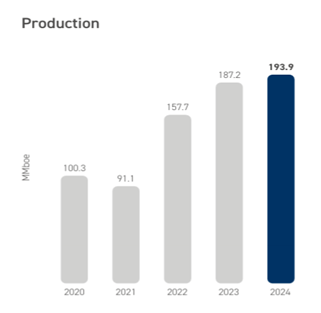

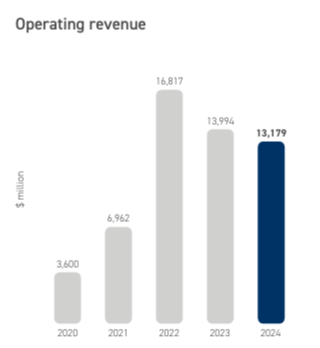

Woodside Energy (ASX:WDS) have been a pioneer of the oil and gas industry in Aus since their beginnings in 1954, when they started exploration and drilling for oil near the small Victorian town of Woodside. To commissioning Australians largest ever LNG resource The North West Shelf off the northern cost of WA and exporting Aus first LNG cargo. Since their humble beginnings, WDS has grown into a global oil and gas producer and explorer with a market cap of AU$40bn, at the time or writing, with revenue of US$13.1bn and record production of 194MMboe in FY24.

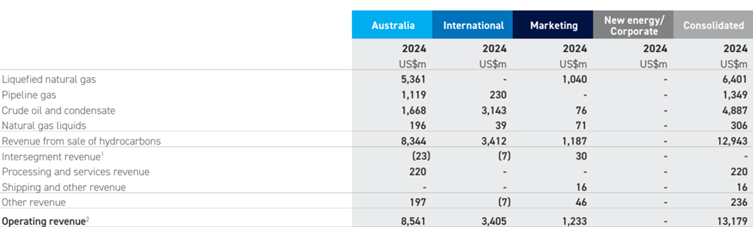

WSD generates its sales, earnings, and profits through four business segments, which are Australia, International, Marketing, and New Energy/Corporate. With the Australian business segment, the largest, producing the bulk of revenues and profits. In FY24 the Australian segment contributed US$8.5bn or 64% of FY24 operating revenue of US$13.1bn.

The corner stone of WDS’s business is the production of natural gas liquids for exports to customers for energy generation.

On 1st June 2022 WDS merged with BHP’s petroleum business to create the largest listed energy company on the ASX and a top 10 energy producer globally. This was done for the consideration of 914m new shares in WDS to BHP shareholders and doubled the amount of WDS shares on issue.

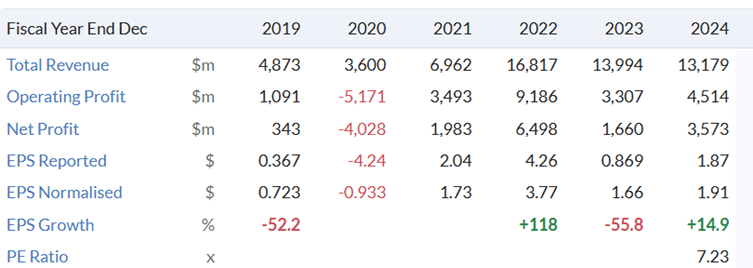

Since the merger WDS has managed to increase their production of oil and gas substantially. With sales, earnings and profits fluctuating with higher costs and a rising and falling oil price. WDS had an average cost of US$8.10boe, while receiving average revenue of US$63.60boe for FY24.

I would also encourage anyone reading this, to peruse WDS website to fully understand the impact they have had on Australia’s oil and gas industry and to understand the true scale and size of their operations, as I am providing a high overview of the company.

WDS have a global production, development, and exploration footprint:

Producing Projects:

- Scarborough Project: Offshore Western Australia, producing LNG and pipeline gas, with a domestic gas commitment.

- Pluto LNG: Includes Pluto Train 1 and Train 2, processing gas from Scarborough and other sources.

- North West Shelf (NWS): Produces LNG, pipeline gas, and condensate, with domestic gas commitments.

- Wheatstone: Produces LNG and domestic gas, adhering to domestic gas policies.

- Sangomar Field (Senegal): Achieved first oil production in 2024 under a production sharing contract.

- Trion Project (Mexico): Deepwater oil development targeting first oil in 2028.

- Browse to NWS Project: Proposed development of Browse Basin gas fields with CCS integration.

- Greater Sunrise Project: Gas and condensate fields between Australia and Timor-Leste, with ongoing negotiations.

- Liard Project: Unconventional gas field in Canada, exploring LNG export options.

Exploration Projects:

- Australia: Exploration in the Browse Basin, Carnarvon Basin, and other gas-prone basins for LNG production and domestic gas supply.

- Africa: Includes Senegal, Egypt, and the Republic of Congo, targeting offshore oil and gas reserves.

- Americas: Exploration in the Gulf of Mexico, Trinidad and Tobago, and Canada, including unconventional gas fields like the Liard Basin.

New Energy Projects:

- Beaumont New Ammonia Project: Located in Texas, USA, focusing on lower-carbon ammonia production.

- H2OK Hydrogen Project: Delayed to prioritize Beaumont.

- H2Perth Hydrogen Facility: Refocused on liquid hydrogen production.

- NeoSmelt Pilot Plant: Electric smelting for direct reduced iron in Perth.

StockRank:

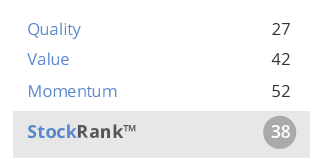

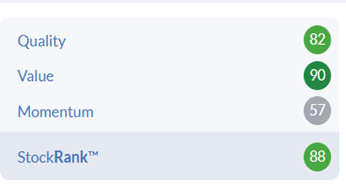

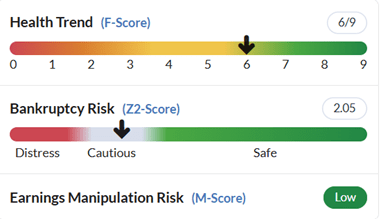

WDS has improved its StockRank numbers substantially since the merger in FY22 and currently has a StockRank of 88, up from 38 in FY21. Apart from increasing the dollar amount of revenue, earnings, and profits. The consistency of all three and WDS margins and returns are not much different to before the merger, more on this later. The main drivers of WDS improved StockRank is the increase in their quality score rising from 27 to 82. This has been due to the improvement in WDS’s health tread, and bankruptcy scores and the lowering of their gearing ratio, more on these later too.

June FY21 Before BHP Merger

May FY25 Post BHP Merger

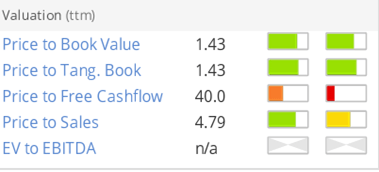

The significant increase in WDS’s value figure from 42 to 90, has been due to the improved valuation ratios post-merger. This has been due to WDS’s share price returning to the same price band before the merger while increasing their asset base, sales, earnings, and cash flow because of the merger. Post merger WDS shares hit a high of $35.5 and at the time of writing were $21.43.

June FY21 Pre-Merger

FY25 Post Merger

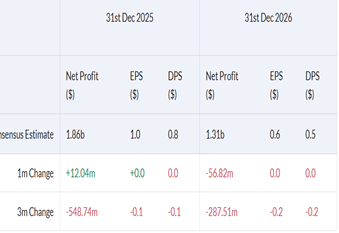

Furthermore, consensus estimates have revenues and profits decline in FY25 and FY26. Based on this and the inconsistent financial performance of WDS, I would be expecting to see their StockRank numbers decline over the next 18-months.

Financials:

As noted above the merger increased the absolute monetary figures and oil and gas production of WDS, but in terms of increasing margins, returns, cash flow and consistency of their financial performance it has not achieved any of these yet. This is evident when looking at operating margin, ROA, ROCE, ROE, and operating cash flow pre and post-merger. Where all these ratios and margins have remained in a similar range and have been inconsistent.

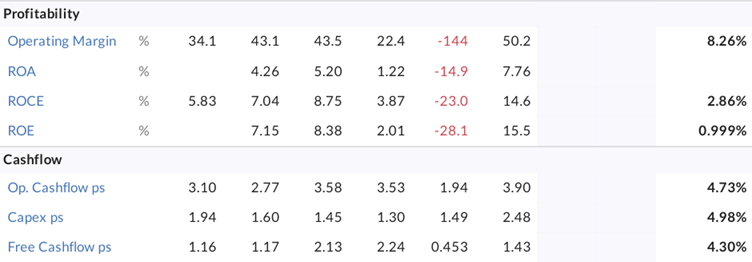

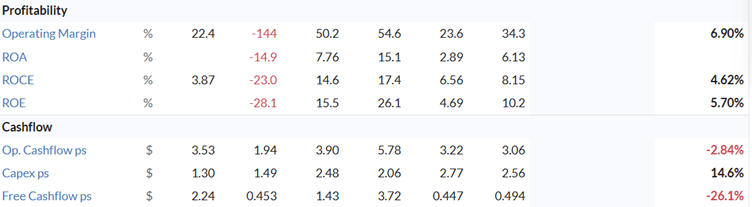

A large part of this inconsistency is due to WDS being a price taker and exposed to the oil price and its fluctuations and cycles. Aa the oil price is a major factor in determining gas prices.

Profitability and Cashflow FY2016-2021 Pre-Merger

Profitability and Cashflows FY2019-2024 – Years FY2022-2024 Post Merger

FY22 FY23 FY24

The main reason WDS’s health tread and bankruptcy risk scores have increased is due to the poor financial performance in FY20 and WDS returning to profitability again in FY21. WDS also reduced their gross gearing ratio from 62% in 2021 to 33% in 2024. Bearing in mind that due to the merger resulting in an increase in shareholder equity. The absolute debt figure has increased but due to the increase in shareholder equity the gearing ratio has decreased.

June 2021 Pre-Merger

May 2025 Post-Merger

WDS does pay a substantial dividend with a dividend yield of 8.35% in FY24. This is due to WDS dividend policy aiming to paying out 80% of net profits. Given WDS’s assets are diminishing. As they extract oil and gas from them each year, they become less valuable and their high payout ratio. It will be difficult for WDS to significantly increase shareholder equity and therefore create value for shareholders over the long-term.

It is also evident when looking at WDS’s capex ps that it has increased since the merger, which is expected when you double the size of your business, and you are in the business of oil and gas exploration and production. Reading through WDS’s reports and quarterly updates, they note that they have gone through a capex intensive cycle developing and bring new projects online and that this cycle will ease as more projects come online from now and until 2030.

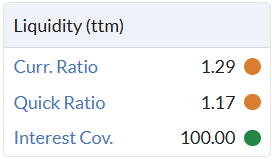

WDS’s cash and asset liquidity ratios have not improved with the merger either, but interest coverage has increased substantially. However, given their size, ability to reduce or not pay dividends, access to debt and equity markets to raise capital and at the end of FY24 they had US$4.1bn cash on hand. I don’t have any concerns with WDS’s ability to remain as a going concern. I would caution though, for a company of this size and their ability to produce cash flows. Their liquidity ratios should be a lot better than they are and I would be expecting them to improve as they bring more development assets online.

Share Liquidity and Ownership:

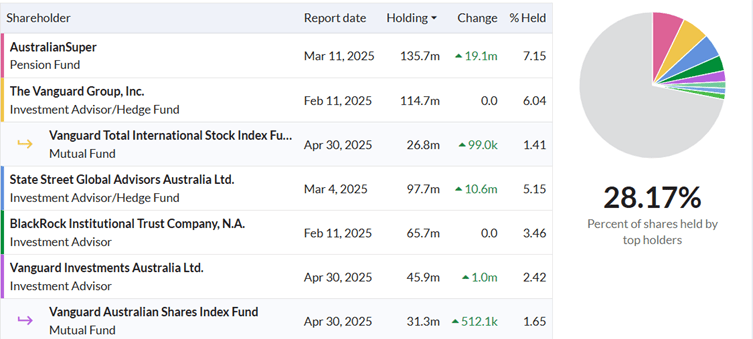

At the time of writing WDS had a market cap of AU$40bn with 1.8bn shares on issue. Of which, 99.9% are classified as free float and can be traded. It is worth noting that before the merger WDS had 927m shares on issue. However, there are some heavy hitters on the top shareholder list and the top three are substantial shareholders, holding more than 5% each of the company’s shares. Top shareholders account for 28.17% of all shares issued and can influence the outcome of events that require shareholder approvals.

But being a large blue-chip stock and with nearly 2bn shares on issues and all but 0.1% classified as free float, small DIY investors will have no issues buying and selling or being able to build a substantial position in relative terms.

Outlook:

Here are some key takeaways from WDS FY25 Q1 market update:

WDS delivered strong operational performance in Q1 2025, achieving production of 49.1 MMboe. Revenue reached US$3.3bn reflecting a 13% year-on-year increase, driven by Sangomar’s exceptional production of 78 Mbbl/day and high gas hub-linked pricing.

Key project updates:

- Beaumont New Ammonia Project is 90% complete and targeting startup in H2 2025

- Scarborough Energy Project 82% complete and first LNG cargo is expected in H2 2026

- Trion Project is 26% complete, expecting first oil in 2028

- Post Q1 FY25 Quarterly update – WDS made a FID to develop the 16.5 Mtpa Louisiana LNG project and targeting first LNG in 2029.

Portfolio optimization included the divestment of Greater Angostura asset and 40% stake in Louisiana LNG infrastructure. Marketing efforts resulted in a long-term LNG agreement with Uniper and China Resources Gas, Strengthening Woodside’s global presence. Despite production challenges, WDS maintained operational excellence and progressed major growth projects on schedule and within budgets. Full-year production guidance remains unchanged at 186-196 MMboe.

Furthermore, WDS has noted in their FY24 annual report and presentation they see global demand for LNG is set to grow by more than 50% by 2034. With a predicted 90 Mtpa LNG supply gap occurring by 2034 if current LNG development and exploration levels remain the same.

Also, WDS see themselves as a key cog in the energy transition to net-zero as they will help fill the base load energy gap left by exiting coal powered electricity stations and helping to firm up renewable energy generation. WDS also see opportunities in helping the world reduce its carbon footprint further by producing new energy from low carbon ammonia, hydrogen, and offering carbon capture utilisation and storage facilities and have plans to invest and develop these areas further.

Also, WDS have been focusing on reducing costs, streamlining and divesting non-core portfolio assets, and have a strong pipeline of producing projects coming online over the next 3-4 years and see themselves producing substantial cashflows after these projects come online.

This is most likely why 6 out of the 11 brokers that cover WDS have a buy recommendation with the other brokers all happy to hold. This is despite consensus estimates forecasting revenue and profits to both decline in FY25 and FY26.

Conclusion:

There is no doubt that WDS have positioned themselves to benefit from the increased demand for LNG created by the push to net-zero and given their proven record of being able to develop some of the world’s largest energy recourses into profitable projects. They have the expertise and skills to develop their current pipeline of projects into profitable assets and capture the increased demand for LNG globally.

As noted above, I find it hard for WDS to create significant capital growth for shareholders given their 80% payout ratio, diminishing asset base, and continuous capex requirement need to run a business like this. This is not to say they will not create any value for shareholders, just that most of it will be paid out as dividends, or special dividends. One could even build an ESG investment case for WDS, given the role they will play in the energy transition. Which could be potentially greater, given their future focus on low carbon new energy production.

Disclaimer: Rational Share Investing With Ratios does not hold an AFSL and information on this site should not be considered financial advice, personal or general, and represents the views of the author.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of my holdings at a certain point in time, and the holdings may change over time.

My Research Tool and Data Source of choice is:

Leave a comment