Economic Updates 2023

17th October 2023

It looks like we are near peak rates and inflation, but rates will be higher for longer and the cost of doing business will continue to increase. This will obviously lead to economic growth being more subdued. Evidence of this is already appearing as primary producers are expecting to outlay $75.9bn on production cost for the 2023/24 season, which is only second to last year’s $76.05bn. Household spending on non-discretionary items is starting to fall as the household savings ratio has fallen to levels not seen since 2009. This has led some economist to believe that continued price increase will now start to hit harder and result in less consumption and decreased demand for goods and services.

Ever increasing geopolitical risks such as the slowdown in the Chines economy due to debt issues in their property market, war and conflicts between Russia and Ukraine and now Israel and Palestine continue to cast uncertainty over the global economy and keep pressure on energy and fuel prices. With the current Israel and Palestine conflict having the real potential to expand as surrounding oil producing nations may get involved.

The WTO has lowered their 2023 trade forecast and left 2024 at 3.3% and have concern that world trade may be starting to fragment due to COVID disruptions, geopolitical conflicts, and the increasing number of more localised trading packs and blocs being signed, as countries look to reduce reliance on China for goods and critical minerals. This will add costs to supply chains and production of these goods and critical minerals. The USA’s Inflationary Reductions Act is an example of this.

For me the canary in the coal mine is still the unemployment rate. The labour market is still tight with low unemployment of 3.7% when compared to the long-term average of circa 5%. The RBA has signalled they want the jobs rate as low as possible while returning inflation back to its mandated level of between 2-3% and has forecast this to occur in 2025. Any significant increase in the unemployment rate from here will signal a definite slowdown in the Australian economy is occurring and visa versa if unemployment continues to remain low. The RBA has signalled they are comfortable with where headline inflation is but are concerned about sticky services inflation driven by higher inputs and labour costs.

For me the Elephants in the room is the continued big spending (debt) and big Governments run state and federally. Both state and federal governments continue to spend and barrow like drunken sailors and the only way to fund this is through higher taxes, charges, and royalties, which we are already starting to see. This just adds to costs of living and doing business. The rush to decarbonise the economy is increasing energy costs for households and business and if it continues will add further cost to households and businesses, if stop gap measures are not implemented. To have significant economic growth, affordable power is critical, currently, we are pulling out all stops just to keep the power on yet alone allow for future growth; and finally, the lower AUD will increase the cost of imports/goods adding further costs to households and businesses. A worst-case scenario could be a large slowdown in the Chinese/world economy which would negatively impact our exports and cause the dollar to fall further at which point the RBA has no choice but to increase interest rates to support the dollar.

In closing, if the status quo remains then we a moving to a higher cost higher rates environment which will lead to subdued growth and lower asset prices for some time.

Bibliography

Some of the driving forces behind inflation remaining higher in Australia are:

Government at all levels Federal, State, and Local show no sign of getting smaller and if anything, it is the opposite. This will continue to add cost and red tape to… well doing anything really; and the best way to fund this continued expansion of the public service will be through increased taxes and debt, which is funded by the taxpayer. So, I would not be expecting the planned stage three tax cuts or any tax relief for businesses or households anytime soon. Both sides of government have shown little appetite for tightening the purse strings, with both sides prepared to talk tough about running a surplus, paying down debt etc, but having very little political backbone when it comes to doing anything.

Post COVID and Trump, nationalism has increased and there is an increase in trading blocs and packs at the expense of world trade and globalisation. Whether you see this as a good or bad thing, does not change the fact that this adds costs to trade, as tariffs and subsidise are incurred, either increasing the costs of our goods and services, making them less competitive on the world stage or increasing the costs or imports, therefore increasing the costs for consumers, households, and business.

Government policy towards decarbonisation and industrial relations, and once again whether you see this as good or bad does not change the fact that this is and will continue to increase the cost of energy and doing business, with these costs passed on to (yes you guessed it) us the consumer again.

Episode #92: Is another rate hike still imminent?

In the last week, we saw the RBA leave interest rates on hold for the fourth month in a row, against the backdrop of increasing uncertainty around political developments in the US and geopolitical risks concerning China. AMP’s chief economist Dr. Shane Oliver explores the outlook for interest rates amid the further softening of the jobs market, falling jobs vacancies and rising levels of mortgage stress.

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.10 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.00 per cent.

Interest rates have been increased by 4 percentage points since May last year. The higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so. In light of this and the uncertainty surrounding the economic outlook, the Board again decided to hold interest rates steady this month. This will provide further time to assess the impact of the increase in interest rates to date and the economic outlook.

Inflation in Australia has passed its peak but is still too high and will remain so for some time yet. Timely indicators on inflation suggest that goods price inflation has eased further, but the prices of many services are continuing to rise briskly and fuel prices have risen noticeably of late. Rent inflation also remains elevated. The central forecast is for CPI inflation to continue to decline and to be back within the 2–3 per cent target range in late 2025…

https://www.rba.gov.au/media-releases/2023/mr-23-25.html

Treasury Yields Reach Levels Not Seen in a Decade

The Federal Reserve’s signal that interest rates would stay higher for longer caused bond yields to spike to their highest levels in more than a decade, and prompted a stock market selloff. Investors are worried a longer period of elevated interest rates will weaken the economy.

The 30-year Treasury bond yield rose to 4.55%, the highest level since 2011 and its biggest one-day jump since June 2022. The 10-year Treasury yield was 4.479%, the highest since 2007. The two-year yield rose to 5.148%, the highest since 2006.

https://barrons.cmail19.com/t/j-e-sctuht-iiudjkuyul-r/

The high price of running a farm has been revealed, with producers predicted to outlay $75.9 billion on production costs in 2023-24, according to ABARES.

That amount is the second highest on record, following the $76.05bn spent in 2022-23, $68bn in 2021-22, $58bn in 2020-21 and $54bn in 2019-20, as supply chains broke and input costs increasingly spiralled due to the Covid pandemic, war in Ukraine and inflation.

The global average price of crude oil in August 2023 was still up 38% compared to the average of 2019, while natural gas prices in Europe were up 133%. Increased storage capacity for natural gas in European countries should prevent extreme volatility in energy prices this winter, but prices could still rise if demand exceeds supply for other reasons, including cold weather or problems with energy infrastructure.

https://www.wto.org/english/news_e/news23_e/tfore_05oct23_e.htm

Evidence of fragmentation Economic and political tensions between the United States and China – the world’s two largest economies – have been building for several years, leading to the imposition of numerous tariffs. These measures have sparked some changes in international trading patterns, but evidence that they have thrown globalization into reverse remains limited. One indicator of the extent of global supply chains is the share of intermediate goods in world trade. Estimates of this share are shown in Chart 10 with fuels excluded from the calculation due to their price volatility. In the fourth quarter of 2022 the ratio fell firmly below 50% and has remained there through the first half of 2023. The shift is not dramatic: as measured by the average of exports and imports, the intermediate goods share has fallen to 48.5% in the first half of 2023, compared to an average of 51.0% over the previous three years. Whether the decline is due to geopolitical tensions or the recent global economic slowdown is unclear. Whatever the reason, the data suggest that goods continue to be produced through complex supply chains, but that the extent of these chains may have reached their high-water mark.

https://www.wto.org/english/news_e/news23_e/tfore_05oct23_e.htm

The WTO furthermore expects real world GDP to grow by 2.6% at market exchange rates in 2023 and by 2.5% in 2024, as set out in the WTO’s “Global Trade Outlook and Statistics — Update: October 2023.”

World trade and output slowed abruptly in the fourth quarter of 2022 as the effects of persistent inflation and tighter monetary policy were felt in the United States, the European Union and elsewhere, and as strained property markets in China prevented a stronger post COVID-19 recovery from taking root. Together with the consequences of the war in Ukraine, these developments have cast a shadow over the outlook for trade. The trade slowdown appears to be broad-based, involving a large number of countries and a wide array of goods.

Trade growth should pick up next year accompanied by slow but stable GDP growth. Sectors that are more sensitive to business cycles should stabilize and rebound as inflation moderates and interest rates start to come down. However, signs are starting to emerge of supply chain fragmentation, which could threaten the relatively positive outlook for 2024. For example, the share of intermediate goods in world trade, an indicator of global supply chain activity, fell to 48.5% in the first half of 2023, compared to an average of 51.0% over the previous three years. Furthermore, the share of Asian bilateral partners in US trade in parts and accessories — a key subset of intermediate inputs — fell to 38% in the first half of 2023, down from 43% in the same period of 2022.

https://www.wto.org/english/news_e/news23_e/tfore_05oct23_e.htm

Largest quarterly fall in the terms of trade since June 2009. The terms of trade fell 7.9% due to export prices (-8.2%). A warmer northern hemisphere winter resulted in high European inventories of coal and liquefied natural gas, reducing demand and prices for these commodities. Prices for iron ore also fell due to reduced demand from China’s construction and manufacturing industries. Import prices recorded a small fall of 0.3%.

Growth in domestic demand prices remained elevated, but declined off their peak in mid 2022 following an easing in demand and global supply chain congestion. Prices for household consumption increased 1.2%, with a strong contribution from rental prices in the tight rental market. Prices for capital investment (+1.3%) also rose, impacted by the depreciation of the Australian dollar.

The household saving ratio declined from 3.6% to 3.2%, the seventh consecutive fall and the lowest level since June 2008. Savings fell as the rise in nominal household consumption outweighed a softer rise in gross disposable income.

Household spending (+0.1%) slowed further this quarter, impacted by pressures on household budgets from inflation and interest rate rises. These pressures have resulted in a continued shift away from discretionary spending towards essential categories.

Discretionary spending fell 0.5%, the third consecutive fall. The decline was led by recreation and culture (-2.5%) and furnishings and household equipment (-2.5%). Spending on transport services (+3.2%) and hotels, cafes and restaurants (+0.2%) continued to increase, but at a subdued rate compared to prior quarters. Partly offsetting the weakness was purchase of vehicles (+5.8%), with vehicles delivered to households this quarter after quarantine delays at ports.

Essential spending rose 0.5%, driven by rent and other dwelling services (+0.5%), electricity gas and other fuel (+2.2%) and insurance and other financial services (+0.6%). The rise in electricity, gas and other fuel reflected stronger demand for heating following a cooler than usual Autumn.

Increased military spend – (why I like some stocks with exposure to military contracts) Total gross fixed capital formation rose by 2.4 per cent. Both public and private investment rose.

“The growth in public capital was driven by health and transport infrastructure investment. National defence investment also contributed to growth, rising by 16.2 per cent.”

https://www.abs.gov.au/media-centre/media-releases/australian-economy-grows-04-cent-june-quarter

Interim Results FY23

15th February 2023

I don’t have many hard rules when it comes to share investing, but one is “no buying or selling during reporting periods “. I like to wait for the dust to settle to avoid making any rash decisions. Now that brings us to the current interim half-yearly reporting period. Company results to date, are what you would expect given where we are in the economic cycle and after 9 straight cash rate increase, with the prospect of a few more to come.

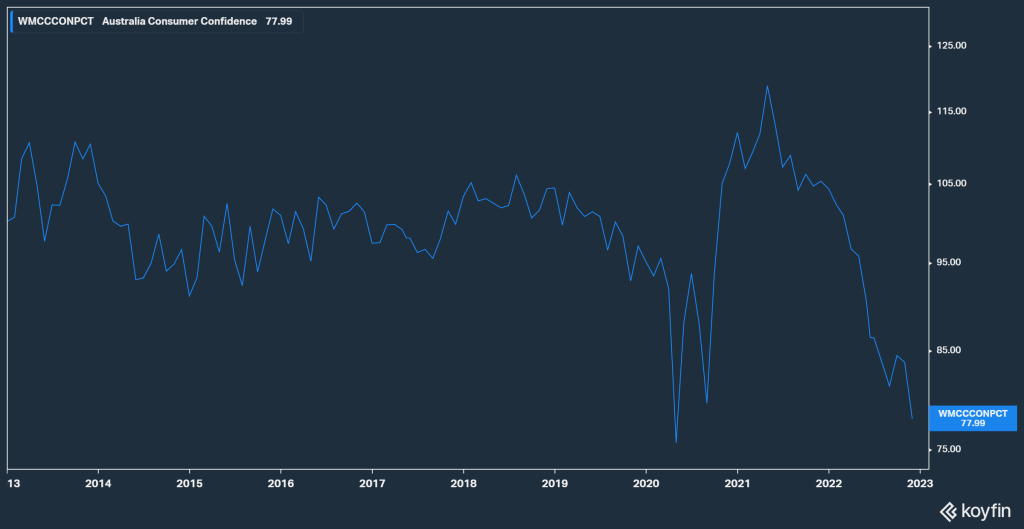

Most of the retailers who have reported so far (JB HiFi, Brevilli, Temple & Webster) have seen sales flatline or decline in the first two months of 2023. Even Nick Scali was cautious about the second half of FY23. James Hardie came in with its third earnings downgrade, on the back of higher costs and declining housing starts across the US and Aus. These results tie in with the latest Westpac Consumer Sentiment index release. Which has fallen to near all-time lows, with only worse readings during recession. Consumers have reported intense pressure on finances, with this most prevalent with mortgage holders. On top of this, there are some 800,000 fixed rate mortgages set to end by the midway point of the year. This is expected to weigh on consumer spending and confidence further. Unemployment still remains low at 3.5% and for me this is the canary in the coal mine and one of the big drivers of inflation. It will be interesting to see what the next labour force read will be on the 16/02/23 and if any of the global IT layoffs of late have caused any issues here in Aus.

All this is pointing to a softer second half of FY23 for many listed companies and the ASX overall. With the standout performers most likely to come from commodity producers, miners, healthcare and possibly one or two in the banking sector.

Economic Outlook For 2023 and Beyond

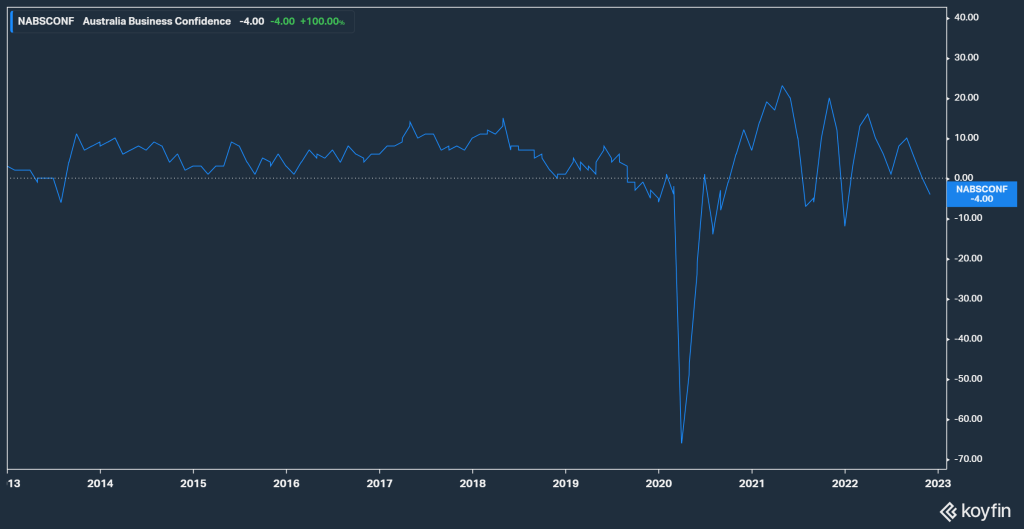

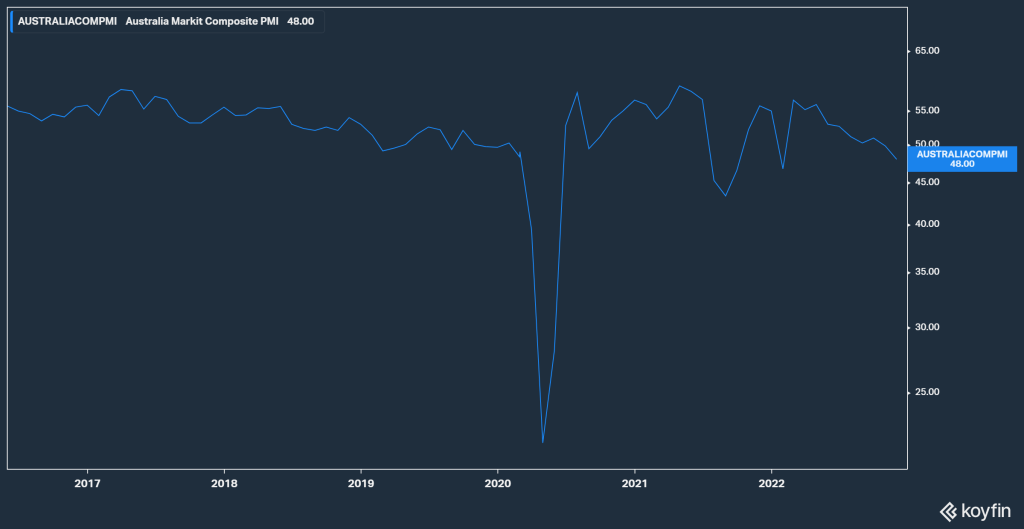

Looking at the current state of play, it would appear we are set for a higher inflationary environment, post pandemic. The good news is that it looks like inflation is stabilising with most forecasts expecting inflation and interest rate rise to peak in early 2023 and then to ease thereafter. This is a result of commodity, gas and oil prices rolling off their pervious highs, increased economic activity in China as they ease COVID restrictions, helping to reduce supply chain and inventory pressures. Furthermore, there is a softening of economic indicators such as business and consumer confidence, and domestic and global PMI’s. All this is indicating that demand for goods and services are normalising as supply chains start to return to post pandemic capacity.

Some of the driving forces behind inflation remaining higher in Australia are:

Government at all levels Federal, State, and Local show no sign of getting smaller and if anything, it is the opposite. This will continue to add cost and red tape to… well doing anything really; and the best way to fund this continued expansion of the public service will be through increased taxes and debt, which is funded by the taxpayer. So, I would not be expecting the planned stage three tax cuts or any tax relief for businesses or households anytime soon. Both sides of government have shown little appetite for tightening the purse strings, with both sides prepared to talk tough about running a surplus, paying down debt etc, but having very little political backbone when it comes to doing anything.

Post COVID and Trump, nationalism has increased and there is an increase in trading blocs and packs at the expense of world trade and globalisation. Whether you see this as a good or bad thing, does not change the fact that this adds costs to trade, as tariffs and subsidise are incurred, either increasing the costs of our goods and services, making them less competitive on the world stage or increasing the costs or imports, therefore increasing the costs for consumers, households, and business.

Government policy towards decarbonisation and industrial relations, and once again whether you see this as good or bad does not change the fact that this is and will continue to increase the cost of energy and doing business, with these costs passed on to (yes you guessed it) us the consumer again.

Here are my two cents on the energy issue: I think the main issue round the energy debate is based on time frames. With energy companies saying we have spent billions of dollars and decades building and developing the energy market here in Australia based on policy of the day and the current government of the day making decisions and policy based on a four-year election cycle. With energy companies saying, if you pull the rug out from underneath us and cap the price, then their needs to be some type of compensation and we cannot guarantee supply if you keep changing the rules. Most of the big energy suppliers are onboard with the energy transition and have plans and are making plans to phase out fossil fuels and move towards greener and carbon neutral energy supply. But they have billions of dollars invested in legacy fossil fuel mines and infrastructure and currently we still get nearly 70% of our energy from coal. So, this issue will not be solved in a four-year term of office and needs a long-term agnostic energy mix approach, rather than jamming intermitted short-term wind and solar into an old legacy energy network.

Higher inflation will mean higher or normal level of interest rates, depending on how you look at it, and will most likely result in lower asset prices and consumption of goods and services as consumer and business borrowing limits and disposable income will be reduce due to higher cost of servicing debt. With this already occurring, as house price having come off their highs and expected to decline some 15-20%. This should also be reflected in lower PE valuations on the stock market, with poor performing stocks being punished by investors, but stocks that do well (that actually have cash flow and make a profit) attracting investors. Having said all this, I’m still optimistic that the economy will continue to hold up well and economic growth will continue after stabilising or possibly contracting in 2023, with a technical recession on the cards. Bearing in mind, a technical recession being a good outcome, as this would most likely indicate that the inflation jeannie is back in the bottle and the RBA indicating it will be happy to loosen monetary policy once again. The most closely observed indicator from here on, is the jobs rate. As the banks have indicated this is the one figure they are watching, because in their minds, as long as you have a job you will keep paying your home loan off. So, all in all, I don’t think we will be shooting the lights out economically anytime soon, but they will most certainly stay on and start to get brighter as 2023/24 roll on.

Disclaimer: Rational Share Investing With Ratios does not hold an AFSL and information on this site should not be considered financial advice, personal or general, and represents the views of the author.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of my holdings at a certain point in time, and the holdings may change over time.