Buy Date: 8th April 2024 | Valuation

MYG FY24 Expectations

12th June 2024

Introduction:

Mayfield Group Holdings Limited (ASX:MYG) reverse listed on the ASX in 2020 and assumed control of Stream Group and at the time of writing had a market cap of $71m, EV of $64m, and had 90m shares on issue with 62% classified as free float. Lindsay Phillips is their largest shareholder with a 45% holding in the company. He also sits on the MYG board as a non-executive director. MYG reported revenue and profits of $77.8m and $5.8m respectively in FY23.

MYG owns a portfolio of complementary, innovative companies in the provision of electrical and telecommunications products and services. They manufacturer custom electrical switchboards, kiosks and transportable switchrooms, and supplier of related services, for critical electrical infrastructure. A niche provider of wireless telecommunications and power quality solutions. End-to-end capabilities in engineering, integration, construction, project management and whole-of- life support services to renewables, mining, oil & gas, infrastructure, defence, utilities & essential services.

MYG operate as a single business segment for reporting purposes, with the group comprising of three businesses Mayfield Industries, Mayfield Services, and ATI Australia. Total revenue comprises of the sale of purchased products, revenue from services, and revenue from manufacturing products.

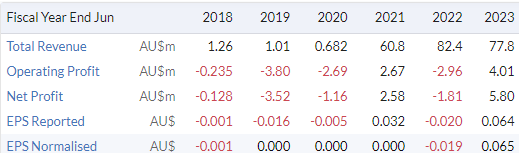

Financials:

Since their reverse listing in FY20, MYG have managed to increase sales, earnings and profits. The decline in sales from FY22 to FY23 was due to MYG focusing and expanding their manufacturing capabilities. Which according to MYG is lower revenue generating but higher margin. Which is reflected in their operating profits and net profits increasing.

To date MYG’s has been unable to produce consistent earnings and profits but when they have, they do produce very respectable returns and margins for a services/manufacturing business. This can be seen in their return on equity, assets and capital being mostly above 10% or higher.

Also encouragingly to see is MYG’s ability generate operating and free cashflows, which have started to flow since FY22. This is a good sign, as it means MYG’s business is generating sufficient cashflows to fund their own capex, dividends, and growth.

This is reflected in MYG having a gross gearing ratio of 6.2%, interest coverage ratio 19. Indicating MYG are conservatively geared and will have no issues funding debt repayments. Further evidence of good asset liquidity is MYG’s quick ratio of 1.4 and their stock turnover ratio of 14.9. This is indicating MYG can meet their short-term liability’s and they are turning over their inventory, which is critical for a manufacture.

Outlook:

In their HY24 report, MYG reported revenue of $38m down from HY23’s $42m. However, they did report an increase in net-profit. Which was up from $1.9m in HY23 to $2.7m in HY24. Other encouraging points from their HY24 report were, net cash from operating activities increasing from $3.5m to $7.0m and MYG repaying $1.8m of borrowings. This help reduce interest and finance costs by half to $93k in HY24. Finally inventory levels remained stable at $2.2m, down slightly from HY23’s $2.5m.

MYG provided little forward guidance in their HY24 report but it does provide a little insight into their operations:

“The revenue decreased from the previous period because of a deliberate focus on manufacturing opportunities that offer higher profit margins. However, this decrease was partly offset by an increase in revenue from our telecommunications and power quality products and services, which had lower profit margins.

Despite having a strong order book, our revenue was adversely affected by client-induced delays that limited our operational activity. Nevertheless, these impacts were mitigated by satisfactory margins that improved throughout the half-year. Our manufacturing operations in Henderson, WA, are experiencing promising growth due to increasing demand. To accommodate this surge, we have planned further investments to enhance our capacity in the second half of 2024 and in 2025.”

What I’m Expecting and Want to See:

Based on the above commentary from MYG and their HY24 results. I am expecting to see a material increase in revenue, earnings, profits and cash flow in FY24, all things being equal. I would also like to see margins from non-manufacturing parts of their business return to previous levels.

Given MYG are looking to increase their manufacturing capacity, capex spending in FY24 and FY25 should increase inline with this.

MYG is a small cap stock and has low share liquidity and a major shareholder holding 45% of stocks on issue. As such I have kept my shareholding small and will look to keep it small relative to my other holdings. The large shareholding by a director pretty much gives the board control of the company and shareholders are just along for the ride. But given MYG’s prudent financial management to-date, it does look like the board are on the same side as shareholders. As such, and given the business currently produces health cash flows, returns on equity, assets and capital. I am looking for the board to keep managing the business the way they are.

Another thing to note is that since 2020 average shares on issue have reduced from 245m to 91m. MYG have done this via share buy-backs. Given this, it would not surprise me at a later date MYG implement a much more aggressive growth strategy by increasing capacity and looking at M&A opportunities. With this new strategic direction being funded by equity, resulting in more shares being issued.

Conclusion:

MYG is not without risk due to their low share liquidity, large shareholding by a director, and other business risks such as weather, cost blowouts, and contract disputes adversely impacting earnings and returns.

However, given the tailwinds facing some of the sectors MYG service, their improving financial and prudent performance, and MYG’s ability to produce health returns on equity, assets and capital. They should be able to capitalise on their market position and generate significant returns for shareholders for years to come.

Disclaimer: Rational Share Investing With Ratios does not hold an AFSL and information on this site should not be considered financial advice, personal or general, and represents the views of the author.

My Research Tool and Data Source of choice is: