Buy Date: 23/02/2024 | Valuation

Bisalloy Steel Group

6th March 2024

Bisalloy Steel Group (ASX: BIS) is an Australian steel manufacturer that specialises in designing and producing high-strength steel products for over 40-years. Publicly listed since 2003, BIS offers a range of products including wear-resistant steel plates, military-grade armour, structural steel, and mining equipment. BIS is Australia’s only quench and tempered (Q&T) steel plate producer which serves our mining and defence industries. One of the more notable products from BIS is their Bisalloy Armor steel, which is specifically developed for military applications, with this product being used in our Collins Class submarines and Bushmaster vehicles deployed in the Ukraine conflict.

BIS comprises of two operating segments Australia and Overseas. Their Australian operations manufactures and sells wear-grade and high tensile plate through distributors and directly to OEMs in Australia and abroad. Their overseas operations comprise three entities operating in China, Indonesia and Thailand which distribute Q&T plate as well as other steel plate products.

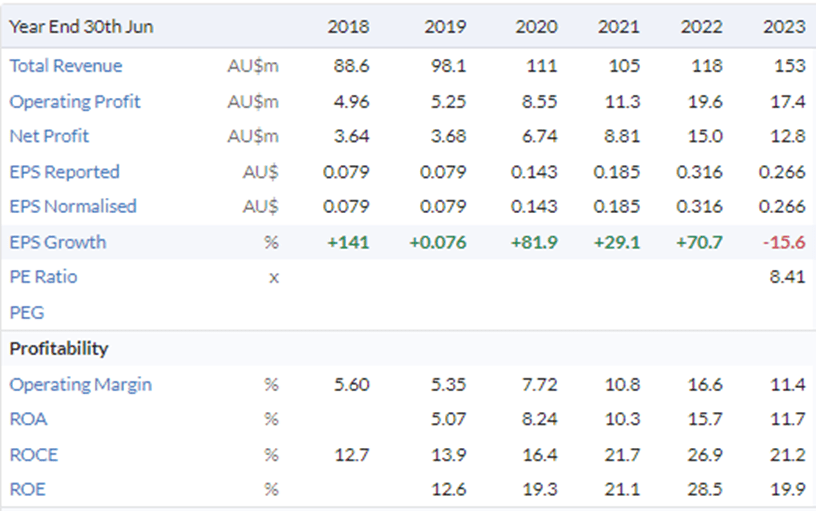

The Australian segment of the business is the largest by far contributing $128.8m to total FY23 revenue of $153.1m, with the overseas segment contributing $24.3m to FY23 revenue. FY23 revenue was up 30% on FY22 but due to higher inputs (gas & electricity) and freight costs earnings and profits declined 7.5% and 14.6% respectively in FY23. BIS has reduced their workshop employees by 20% to help offset rising costs, and further impacting sales was a change to their enterprise resource planning system (ERP) which impacted sales of some products, this has been rectified. Despite these headwinds BIS continues to be a profitable company generating solid returns and paying dividends and will pay a special dividend of 10c per share in November 2023.

Looking forward to FY24 and beyond BIS is continuing with its growth strategy of focusing on the premium grades of Q&T steels, including armour and defence grades while developing the volume growth of other products.

BIS have just released their HY24 interim results where they reported total revenue of $76.6m down 2.3% compared to pcp. But due to lower inputs for the half (mainly lower ocean freight costs) BIS reported a 14% increase in gross profit to $19.4m and an 18% increase in net profit after tax of $8.2m for the half. This resulted in EPS increasing to 17.4c for HY24 up from 14.6c in HY23 and BIS had cash on hand of $651k for the half down from $730K in HY23.

Some commentary from BIS’s interim report sheds further light on the half:

Australian Operation:

“Australian demand for quenched and tempered steel plate remains strong. Our domestic sales were impacted by down-time caused by industrial action as part of our EBA negotiations. We have recovered from the impacts of this disruption, rapidly improving our inventory levels resulting in improved trading. We have also negotiated improved Gas and Electricity contracts commencing 1 January 2024 and these along with reductions in transportation costs will support our Australian margins in H2 FY24.”

Overseas Distribution:

“The Group’s overseas distribution operations in Indonesia and Thailand continue to be profitable. Demand in Thailand has increased in HY24 compared to prior year, however margins have reduced due to the impact of higher product costs and market selling price compression. The Indonesian operation has been impacted by Import License restrictions. Despite the efforts of the Indonesian team, they have not been able to offset this impact in the 6 months. We hope and expect to see this resolved over the coming 6 months, with Indonesian operations returning to normal in FY25.”

Protection Steel:

“Our Protection Steel business continues to be of importance both domestically and internationally. Volumes are up 23% from HY23 and we see this as an area of continued growth through key export markets.”

Overheasds:

“Overheads were in line with expectation, but higher in HY24, driven by planned increases in investment in marketing, people and projects, along with higher legal costs relating to new contracts, lower unfilled positions, and increased incentives due to improved performance.”

On face value this looks like it was a good half for BIS as margins, earnings and profits all increased, all be it on flat total sales. But after going through their HY24 report I do have a few concerns.

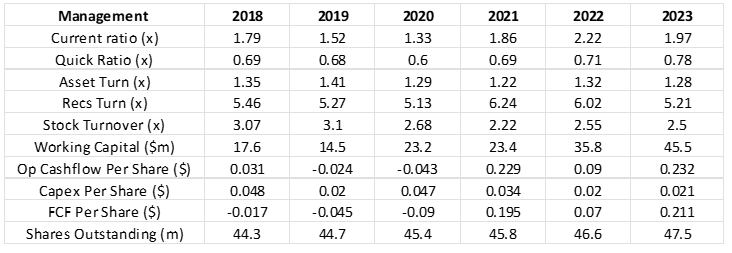

Inventories were up 9% compared to HY23. Due to order phasing and export shipment delays across the half. BIS did note this in their Australian operations and that they have rectified the issue. But come their full year results this is something I will be watching closely.

Furthermore, BIS had negative cash flow from operations of $1m compared to positive $1.1m in HY23 and BIS increased debt levels and drawdown $7.9m of this for the half. They also paid $9.5m in dividends, this included the special dividend paid in November 2023. To helping offset this, BIS did receive a $2.1m dividend from their Chines joint venture, but if it wasn’t for the increase and drawdown of borrowings BIS would not have been able to pay-out the $9.5m dividend. You don’t need to be a accountant to figure out that this is not sustainable. As a business cannot keep generating negative cash flow from operations and borrowing to fund dividends into perpetuity.

Over the past three years BIS has been producing positive cash flows and reduced debt. For me and from here onwards at a minimum before I purchase more shares. I need to see cash flow from operations return to or above previous positive levels, and ideally debt levels stabilises and start to reduce.

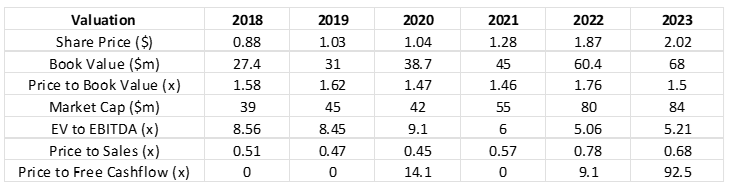

Ratio Analysis

BIS has increased revenue, earnings, margins and profits, while maintaining a flat level of shares outstanding. Which goes someway to explaining why their share price has gone form $0.76 at the start of 2018 to their current price of $2.84 at the time of writing.

BIS has either maintained or improved management ratios and when you are increasing sales, margins, earnings, and profits on the other side of this. You can see why their share price has gone north.

Once again BIS has done all the right things here by shareholders and reduced debt and maintained cash levels.

BIS has been prudent with their dividends and dividend cover has generally been at or close to two times earnings. Meaning BIS has been retaining some profits to be reinvested back into the company.

These are the numbers you like to see increasing or being maintained at current levels. IF BIS can maintain their current asset & equity and earnings and margins ratios while increasing sales, then there is a lot more upside to their share price.

If you are a true believer like myself and thing BIS can keep growing sales and maintian their current margins and raios over the long-term then BIS are cheap. But if you are on the other side of the ledger then at their current share price of $2.84 at the time of writing then they are expensive. I see more upside over the next 5-10 years for BIS and at current levels they are cheap.

Other Observations

This little bit of analysis is why I really like BIS and if they can continue to preform. Is why I see more upside in their share price.

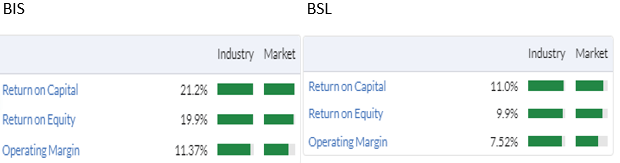

The theory goes that large blue chip stocks trade on a high PE multiple due to their market strength and stability of earnings and profits etc. So, by quickly comparing BIS to BlueScope Steel (ASX: BSL), a David and Goliath comparison, we should see BSL with superior returns and margins.

However, despite their diminutive stature, BIS has higher margins and returns than a company some 80 times larger! Highlighting the quality of their business, products, and their competitive advantage in being Australia’s only Q&T plate manufacture.

Also worth noting, BIS are on the small side of small with a market cap of $133m and 47.5m shares on issue with just over half of issued shares being classified free float and able to be traded. This is mostly due to major shareholders holding 50.1% of the company and the top two shareholders owning nearly 30% of the company. Which makes AGM’s and anything that requires a shareholder vote a forgone conclusion and the ability to get larger parcels of stocks impossible unless further equity is issued.

Outlook

BIS has given little forward guidance apart from they expect the strong profit momentum from HY24 to continue through to the end of FY24 and on the back of inputs falling they are expecting margins to normalise in the second half too.

Conclusion

I like BIS long-term and think there is more upside to their share price if they can return to positive cash flows, maintain their current margins and ratios, while sales continue to grow. But their small cap stature and small number of shares on issue and less being able to be traded does mean buying and selling may not be straight forward. Also, their share price can fluctuate from time to time due to this. But this is what you get when investing in small cap stocks and by taking a long-term view on the company, I am not concerned by short-term price movements.

Disclaimer: Rational Share Investing With Ratios does not hold an AFSL and information on this site should not be considered financial advice, personal or general, and represents the views of the author.

My Research Tool and Data Source of choice is: