Buy Date: 30/10/2022 | Valuation $4.00

Stock Note:

15th February 2024 | Share Price $4.47

After the Holmen Acquisition I’m a willing buyer at $4.00-$4.50. When capital is available.

9th December 2023 | Share Price $3.90

Up 26% on original investment. Will not add to holding at or above $4.00 share valuation. Will look to buy more at or below $3.90, When capital is available.

Reliance Worldwide (ASX:RWC)

4th June 2024

Give it is almost end of financial year, I though I would go through some of the stocks in my portfolio and outline what I would like to see from them in their FY24 annual report, what guidance the companies have given, and what to expect.

First up is Reliance Worldwide (ASX:RWC), at the start on May 2024 RWC reaffirmed forward guidance they had given in their HY24 report back in February 2024.

RWC’s HY24 guidance

Consolidated Group

Consolidated group revenues are expected to be down by low to mid-single digit percentage points compared with pcp. This guidance excludes any contribution from Holman Industries in FY24.

RWC is continuing to target stable operating margins for the full year compared with FY23, with the impact of lower volumes on operating margins to be offset by cost savings.

Operating cash flow conversion in the second half is expected to be above 90% for the period.

Americas

Sales in the Americas are expected to be broadly in line with the pcp, after adjusting for the impact on sales of the closure of Supply Smart.

Operating margins are expected to be higher than for FY23 and consistent with HY24, following the progressive transfer of some SharkBite manufacturing and assembly from Australia to the US.

APAC

APAC external sales, excluding the contribution from Holman Industries, are expected to be down by low single digits.

Intercompany sales will be significantly lower in FY24 following the transfer of some SharkBite Max production to the US.

Operating margins in FY24, excluding the contribution from Holman Industries, are expected to be around one third lower than in FY23 due to lower demand in the Australian market, along with the major changes in manufacturing orientation away from exports to the US.

As disclosed at the time of the acquisition, Holman’s earnings are weighted to the first half of the financial year and therefore are not expected to make a material contribution to FY24 earnings.

EMEA

External sales in local currency are expected to be down by low double-digit percentage points in FY24 versus pcp, consistent with the first half of FY24. Operating margins are also expected to be lower than pcp.

Key Points and Takeaways

RWC report in US$, all $ figures are in US$ unless stated otherwise

RWC reported net sales of $1.24bn in FY23, EBITDA of $276.1m, and NPAT of $139.7m. This resulted in an EBITDA margin of 22% and a NPAT margin of 11.2%. RWC also produced $250m in cash flow from operation. Also, RWC completed the acquisition of Holman in March 2024. According to RWC’s investor presentation 75% of Holman’s revenue (FY23 $180m) is generated in the first half of the FY. As such, the Holman acquisition is not expected to contribute to sales and earnings significant in FY24.

With all this in mind and RWC’s forward guidance, I think consensus estimates for FY24 sales and profits to come in at $1.23bn and $147m respectively is pretty much on the money.

At a business segment level, I will be keeping a close eye on how far margins fall versus guidance. A 1/3rd decline is 33%, which is a large decline and needs to be watched closely.

I want RWC to maintain their prudent dividend policy of distributing 40-60% of annual profits as dividends and share buy-backs and keep paying down debt.

RWC will be able to do this as based on their guidance and their HY24 result they will produce substantially more cash flow from operations than FY23. RWC reported HY24 cash flow from operations $151m. So, I’m expecting RWC to continue their prudent capital management on the back of increased cash flows from operations. RWC informed investors that the $160m Holman acquisition will be 100% funded by their existing debt facility of $1bn, of which $421m was undrawn as of 31st December 2023. As such, I am expecting a small increase in debt levels.

Being a manufacture it is critical RWC manage their inventory levels well. Since the start of FY23 RWC have been reducing inventory levels on the back of inventory building up due to COVID disrupting their supply chains and the need to carry higher levels of inventory to ensure stock was available for sale and distribution. In their HY24 report RWC reported they reduce inventory levels by $51m and are focused continuing to reduce inventory levels for the rest of the FY. This being the case, I will be expecting inventory levels to be lower than FY23. Also working capital should fall on the back of this and should help increase cash flows too.

The Holman acquisition will distort ROA and ROE ratios, as the assets will be on the balance sheet, but RWC will not have a full year of earnings from the business. As such we will have to wait until RWC’s HY25 report to get a better understanding of how the acquisition is performing.

Given RWC cyclical nature, management continuing to buy-back shares, and the construction cycle nearing or at the bottom of a downturn in Aus and the US. RWC represent good value at any price below $5.00.

In conclusion, I’m expecting a flat financial performance from RWC for FY24, which is in keeping with their forward guidance. However, increased cash flows will allow them to continue with their prudent capital management and paydown debt and return capital to shareholders via dividends and share buy-backs.

Reliance Worldwide (ASX:RWC) FY24 Interim Results

24th Feb 2024

RWC reported flat revenue of $589.5m, down 2% for the half. Reported EBITDA was down 19% to $112.6m, with reported net profit down 23% to $51m. All RWC’s business segments reported flat or lower revenue. On face value this doesn’t look like a good result. But we are about to see why cash flow is king.

RWC increased cash flow from operating activities by 61% to $151.6m for the half. This is why when you strip out one of costs for the half RWC’s underlying net profit was $67.7m which is inline with reported net profit for the FY23 half. This large increase in cash flow from operations allowed RWC to reduce net-debt by $138.8m to $394.7m. RWC has a total committed debt facility of $1.0bn with $628m available. This debt facility will also be used to fund the $160m Holman acquisition which is expect to double APAC business segment revenue. When completed, this will be a timely acquisition for RWC as their APAC business segment was the worst performing with net sales down 21% and adjusted EBITDA down 55% for the half. This was due to restructuring part of their manufacturing facilities to the US reducing internal sales, and declining new housing starts in Australia, reducing demand for their products.

RWC maintained their divided policy of distributing between 40-60% of annual net profits and declared a 4.5c dividend for the half, total of $35.6m. The dividend will be broken up into two components. A cash divined of 2.25c and an on-market share buy-back of 2.25c.

A further good sign is RWC reduced net-working capital by $77.2m for the half, more than double the amount they will payout as dividends for the half.

RWC is expecting sales, margins and profits to be down by low signal digits cross the whole business in FY24.

This report sums up why I like RWC, they are doing all the right things for shareholders. Paying down debt, buying back shares, maintain a prudent dividend policy, and continue to make strategic acquisitions that deliver vale for shareholders. And is why despite the flat forecast for FY24 their share price is AU$5.27 at the time of writing, up 70% on my original investment. RWC are a cyclical business due to their exposure to construction and housing and I’m expecting some weakness in their share price from here and see this as a buying opportunity. As when the economic cycle starts to changes and housing and construction starts to improve here and in the US, their share price should follow.

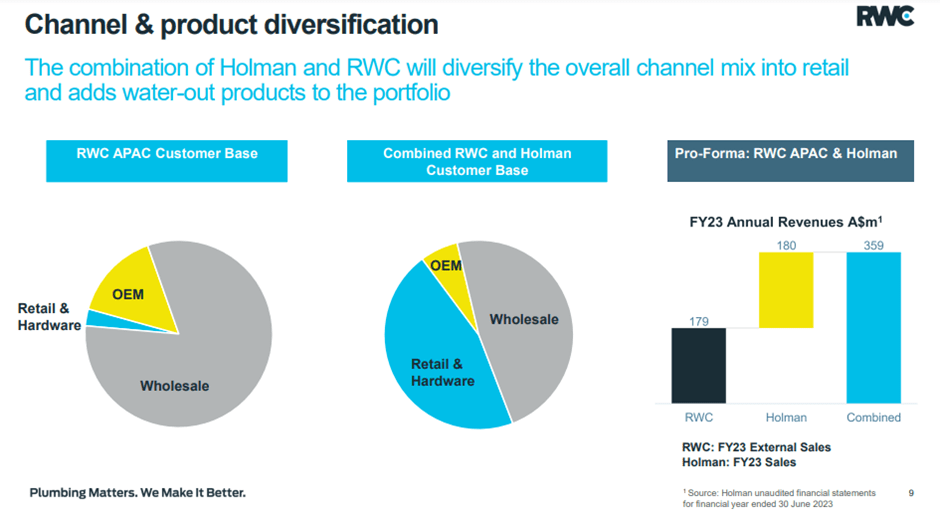

Holmen Acquisition

14th February 2024

I like the look of the Holman acquisition. RWC will fund the $160.0m deal via their existing debt facility. The price tag represents 7 times Holman’s FY23 EBITDA, which is not cheap. So RWC have paid to play here and the acquisition although according to RWC will be EPS accretive in the first year is more of a strategic acquisition than a bolt on one.

The deal will double the size of RWC APAC business segment and substantially increase their retail offering in Australia and expand their wholesale offering too. Doing some rough numbers here. RWC had a profit margin of 11% in FY23. I would expect Holman to be similar. 10% of Holman’s FY23 revenue gives us a $19m profit for the business. Consensus has RWC generating a profit of AU$237m in FY25 adding the $19m form the Holman question gives us a profit of AU$256m. Which equates to EPS of 32c slightly above analyst consensus of 30c for FY25. Using RWC’s forward PE of 15 and applying this to the 32c EPS gives us a share price of $4.80.

HY23 Interim Results FY23

Revenue was up 15% to US$601.3m and volumes were up 11% on pcp. This included a full contribution from EZ-Flo for the half-year, excluding EZ-Flow volumes were down 2% overall. Revenue growth in all regions was due to an average price increases of 8.5% cross the product range. RWC are still indicating high input costs and inflation are continuing to put pressure on margins. EBITDA came in at $128.1m, up 2% on pcp. Reported NPAT was $66.6m up 5% on pcp and they declared an interim dividend of 4.5c. RWC noted that inventory levels were high as a result of a pending new product release and the hangover effects of COVID, and said they will be looking to reduce inventory levels in 2H23. RWC did not provide forward earnings guidance but are expecting cost pressures to ease and the benefits of costs reductions to benefit them for the rest of 2023, but did sight, falling volumes and a potential lack of confidence of consumers to spend on home improvements as areas of concern:

Gross Profit Margin 37% (FY22: 27%)

EBITDA Margin 21% (FY22: 22%)

Profit Margin 10% (FY22: 8%)

Cash Conversion 50% (FY: 23%)

Given the current business and economic conditions this is solid result. Sales are up on lower volumes, due to price increases and the EZ-Flow acquisition. Cost pressures are expected to ease for the rest of CY23, but uncertainty remains round forward trading conditions. There has not been any decline in margins, and a good sign is RWC’s cash conversion ratio has improved from their FY22 annual report. The market has liked this news too, as since adding RWC to my portfolio their share price has gone from $3.12 to $3.64 a share. At this stage I will be holding and waiting for their next quarterly update, and

RWC Analysis 6th Nov 2022

| Earnings &Margins | 2018 | 2019 | 2020 | 2021 | 2022 |

| Sales Per Share $ | 0.97 | 1.40 | 1.47 | 1.70 | 2.15 |

| CFPS $ | 0.10 | 0.17 | 0.30 | 0.26 | 0.11 |

| EPS $ | 0.08 | 0.17 | 0.11 | 0.18 | 0.17 |

| Gross Profit Margin % | 41.2% | 42.1% | 41.1% | 32.9% | 27.1% |

| Cash Conversation % | 61.5% | 52.1% | 97.6% | 58.2% | 23.6% |

| EBITDA % | 16.9% | 23.6% | 21.2% | 26.3% | 22.2% |

| EBIT % | 13.8% | 19.7% | 15.9% | 22.1% | 18.2% |

| NPAT % | 8.6% | 12.0% | 7.7% | 10.5% | 8.1% |

RWC has increased sales revenue from $769m in 2018 to $1.7b in 2022. This can be seen in sales per share increasing from 97c to $2.15 in this time. The increase in sales has resulted in higher profits. With profits going from $66m to $137.4m in 2022, with profits peaking at $140.9m in 2021. However, in 2021 RWC’s earnings and cash conversion ratios stated to decline. This is mainly due to increased input costs (raw materials) and an increase in inventory. Inventory levels have increased as RWC has looked to insulate itself against supply chain issues caused by COVID. In their 1Q update for FY2023, RWC noted: Higher input costs experienced early in 2022, particularly copper, zinc and stainless steel have eased since their peak in mid-2022 which is expected to positively impact operating margins later in FY23. Also, During FY2022 RWC Successfully integrated Ezy-flo and LCL into the company. RWC acquired them for $332m and $28m respectively. LCL is a strategic acquisition as they are Australia’s largest producer of high-quality copper-based alloys and processes both new and recycled materials to produce a range of brass alloys. This secures a major part of RWC’s supply chain, as LCL’s brass operations are located in Melbourne next to RWC’s. Ezy-flo was a bolt on acquisition, as it contributed $124m to revenue in FY2022 and $58m to revenue of $303m in 1Q FY2023, which is up 23% on the pcp. The US is RWC’s largest business segment, accounting for $790.9m of $1.7b of revenue in FY2022. RWC has noted they are seeing a decline in volume in the US and EMEA, but APAC still has rising volumes. RWC has increased their price to help offset the effects of higher inflation, and this has contributed to earnings growth in FY2022 and Q1 FY23.

| Management | 2018 | 2019 | 2020 | 2021 | 2022 |

| Current Ratio | 3.9 | 3.8 | 2.4 | 2.0 | 3.2 |

| Days Debtors | 97 | 77 | 83 | 60 | 57 |

| Days Creditors | 80 | 44 | 53 | 49 | 37 |

| Working Capital ($m) | $239.9 | $329.3 | $310.2 | $235.3 | $408.6 |

| Change in Working Capital | -89.4 | 19.1 | 74.9 | -173.3 | |

| Days Inventory | 96 | 76 | 68 | 53 | 68 |

| Deprecation/Cap Ex % | 55.3% | 71.2% | 191.4% | 138.2% | 97.8% |

| Effective Tax Rate % | 33.5% | 24.7% | 34.2% | 30.7% | 29.9% |

Over the last 5-years, RWC’s management has improved efficiencies and managed the company well. The current ratio of 3.2 is indicating RWC’s short-term assets will cover short-term liabilities, the company has good liquidity. This can also be seen by the days debtors and creditors reducing, thus speeding up the time it takes them to pay their bills and to collect money owing. Further to this point, days inventory has reduced from 96 to 68 days, highlighting they are selling more and turning over their inventory more that 6 times in a year. The increase in working capital has been due to increased levels of inventory due to COVID, aimed at reducing supply chain issues. RWC does have a health capital expenditure program, as they are spending, more often than not, the same or more than they depreciate. A good sign management is not trying to cut corners and keep their operations modernised. Management is not trying any tricky accounting as their effective tax rate is basically the same at the corporate tax rate of 30%. Another good sign management is pretty much straight down the line and being honest with shareholders.

| Debt & Interest | 2018 | 2019 | 2020 | 2021 | 2022 |

| Debt to Equity | 49.8% | 35.3% | 27.1% | 13.4% | 49.3% |

| Net Debt ($m) | $385.3 | $426.1 | $302.2 | $130.4 | $560.1 |

| Interest Coverage Ratio | 8.9 | 9.6 | 9.0 | 32.5 | 19.6 |

| Debt to EBITDA | 5.1 | 1.9 | 1.6 | 0.4 | 1.6 |

| Debt to Cash Flow | 8.2 | 3.6 | 1.6 | 0.7 | 6.6 |

| Financial Gearing | 20.0 | 29.2 | 11.4 | 17.7 | 71.3 |

RWC has access to debt facilities totalling $1.0b with $551m of net debt at the end of FY2022. Despite increasing debt to fund their acquisitions, RWC remains in a very good position and does not look to have over borrowed as debt to equity is still relatively low at 50%. EBIT earnings will cover interest payments more than 19.6 times, it will take 1.6 years for RWC to pay off their debt with EBITDA (once again a relatively low level), and the increase in debt has resulted in some $71.3m in revenue being generated. Debt to cash flow is high, but once again this has been due to the increase in inventory levels, and I would be looking for this to improve in FY2023.

| Dividends | 2018 | 2019 | 2020 | 2021 | 2022 |

| DPS (cents) | $0.04 | $0.07 | $0.05 | $0.10 | $0.10 |

| Payout Ratio % | 51.4% | 41.3% | 43.7% | 53.9% | 55.8% |

| Dividend Cover | 1.9 | 2.4 | 2.3 | 1.9 | 1.8 |

| DY | 0.8% | 2.0% | 1.7% | 1.8% | 2.4% |

RWC has shown financial discipline by maintaining a 50% payout ratio, showing they are retaining profits and reinvesting this back into the company, and is one of the main reasons despite COVID and the increase in inventory, they still paid a dividend in FY21 and FY22. Another great sign that management is on the same side as the shareholder. RWC will continue to pursue its policy of distributing between 40% and 60% of annual NPAT by way of dividends each year. RWC is only able to pay partially franked dividends for Australian taxation purposes due to the geographic mix of its earnings.

| Assets & Equity | 2018 | 2019 | 2020 | 2021 | 2022 |

| Asset turnover | 0.4 | 0.5 | 0.6 | 0.7 | |

| ROA | 4.8% | 10.5% | 8.3% | 17.7% | 14.8% |

| ROE | 5.0% | 9.5% | 6.3% | 12.5% | 11.5% |

RWC has increased its returns on assets and equity since 2018. This correlates with their improvement in management ratios above, is indicating that management is focused on finding efficacies and creating returns for shareholders. The asset turnover ratio is also improving and indicating RWC is generating more revenue from their asset base. An asset turnover ratio of 1 to 1.5 is a good rule of thumb, indicating there is room for improvement here. All things being equal, an improvement in this ratio will generally result in higher ROA and ROE. A point to note on this ratio is, RWC have put their prices up on their products to compensate for the increase in inflation and this will have increased this ratio. As it stands, RWC have generated increased revenues on the back of falling volumes. This is the result on their price increases and is something to keep a close eye on, as this is not sustainable, and volumes will need to stabiles or increase from here for RWC’s share price to remain at current levels.

| Valuation | 2018 | 2019 | 2020 | 2021 | 2022 |

| Price to Sales | 5.5 | 2.5 | 2.0 | 3.1 | 1.9 |

| EBITDA Multiplier | 35.5 | 12.3 | 10.6 | 12.2 | 9.9 |

| Historic PE | 64.2 | 20.8 | 25.4 | 29.3 | 23.2 |

| Book Value $ | 1.68 | 1.78 | 1.8 | 2.01 | 2.08 |

| Price to Cash Flow | 52.9 | 20.3 | 9.4 | 20.1 | 35.8 |

| Share Price $ | 5.36 | 3.50 | 2.87 | 5.22 | 4.04 |

| Market Cap $b | 4.2 | 2.7 | 2.3 | 4.1 | 3.1 |

| EV $b | 4.6 | 3.2 | 2.6 | 4.2 | 3.7 |

RWC traditionally has treaded at a premium when looking at their price to sales, EBITDA multiplier and PE ratios. Their current PE of 18 is the lowest it’s been in the last 5-years. Their price to cash flow ratio has been impacted by the increase in inventory levels, likewise the three previous ratios will have been impacted by RWC’s price increases in the last 18-months. RWC has increased sales on the back of declining volumes due to these prices rises and the Ezy-flow acquisition; and with forecast global growth to decline. RWC’s sales, margins and share price could come under further pressure in the next 6-12 months. Having said this, the price of inputs and supply chain issues look to have eased in the second half of FY2022 and this is looking like it will continue into FY2023; Helping to ease presser on margins and earnings, as new inventory will be sold at higher prices but have lower input costs.

Conclusion

Over the last 5-years RWC’s management has improved efficiencies, increased sales and returns, and have been prudent with their financial gearing and dividend strategies. With all this being aligned with shareholders’ interests of creating long-term value. Through this prudent management, RWC is in a strong position to weather the current economic downturn and benefit when conditions start to improve. Traditionally, their PE ratio has been in the mid to low 20’s. With this in mind, applying a PE ratio of 21 to their FY2022 EPS of 17c, we arrive at a share price of $3.57. At the time of writing, RWC’s share price was $3.06. Based on this basic valuation and the above analysis, I like RWC at is current level. I will use a dollar average strategy moving forward. Where I will buy at the current levels and then wait for a further update and if they surprise to the upside, I will average up; or if they surprise on the downside, I will average down. As based on my analysis, I am confident they can weather the economic downturn and benefit when the cycle starts to improve.

Reliance World (RWC) is on my Watchlist

(26 Oct 2022)

This is a company I like and with the share price at circa $3.00, I’m very interested! Being in the building and construction space, they will experience the ups and downs of the construction industry as it inevitably cycles through its boom-and-bust phases. But this is a good stock to buy and hold through these phases. Management has done the right things by shareholders and has returned excess capital, since listing in 2015 they have not issued more shares, thus not diluted existing shareholders. For a manufacturer in this space, they are conservatively geared with a 60% net-debt to equity ratio. Finally, they have stuck to their knitting and management has not decided to go off and buy a movie studio or start manufacturing EVs, or something daft like this! RWC is involved in designing, manufacturing and supplying of high quality, reliable and premium branded water flow, control and monitoring products and solutions for the plumbing and heating industry. They have stuck to this and have made and acquisition of EZY-flo in the US to expand their offering. The jury is still out on this acquisition and time will tell, if they get it right. Their share price has dived on the back of a poor FY23 first quarter update. Where, like Jim Chalmers and the Labour budget, they said demand is down, costs are up, and margins will get squeezed. I think there is still a bit more pain to come for RWC and this could potentially be buying opportunities and a great way to use dollar averaging to build a position on their share registry. Over the next little period I will look at the numbers more closely and conduct my own valuation… I like the way management run this company and that is why I have put it on my watchlist, I’m happy to back the jockey on this one!

Disclaimer: Rational Share Investing With Ratios does not hold an AFSL and information on this site should not be considered financial advice, personal or general, and represents the views of the author.