By Anton Crabbe 20th July 2025

Executive Summary

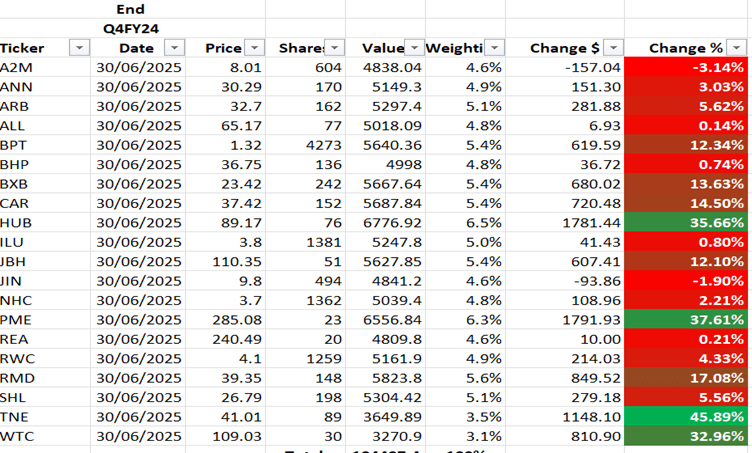

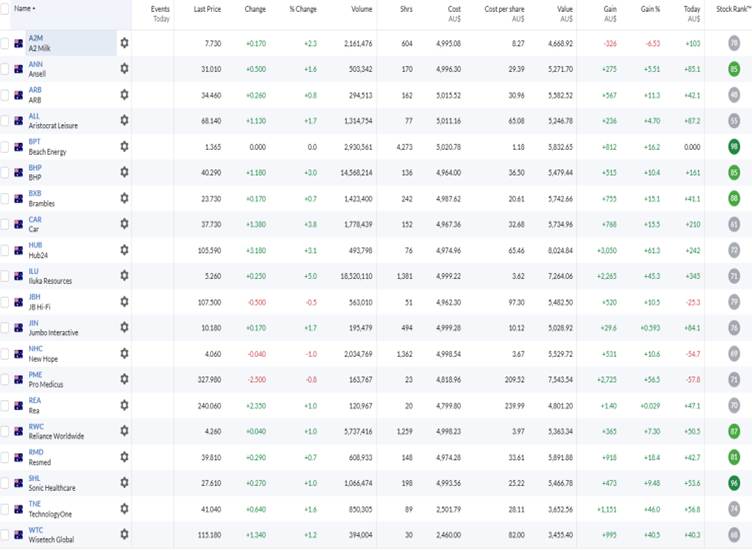

The ASX 300 Portfolio has shown strong performance for the quarter ending 30th June 2025. The top three best-performing stocks were Technology One (ASX:TNE) with a 45.89% increase, Pro Medicus (ASX: PME) up 37.61%, and HUB24 (ASX: HUB) up 35.66% 1. Conversely, the bottom three performers were The a2 Milk Company (ASX: A2M) down -3.14%, Jumbo Interactive (JIN) down -1.90%, and Aristocrat Leisure (ASX:ALL) up 0.14%.

Overall, the portfolio is up 18.59%, outperforming the ASX All Ordinaries, which is up 13.16%. During the quarter, Telix Pharmaceuticals (ASX: TLX) and James Hardie (ASX: JHX) were removed from the portfolio due to high debt levels and regulatory/governance issues, respectively. The portfolio maintains flexibility with no limit on cash holdings and aims for a 15% total return per annum over the long-term.

Strategic decisions included reducing holdings in HUB24 (ASX: HUB), Technology One (ASX: TNE), and Wisetech Global (ASX: WTC) to manage risk and take profits. New additions to the portfolio, Aristocrat Leisure (ASX: ALL) and ARB Corporation (ASX: ARB), meet the investment criteria and have been consistent performers.

In conclusion, the portfolio’s performance has been positive, and future capital deployment will be guided by the established investment criteria to maximize returns and manage risk effectively.

Investment Criteria

Inception Date 15th April 2025

Sector and Industry Agnostic

Aiming for a 15% total return p.a. over the long-term.

Started out with 100k equal weighting invested over 20 ASX300 Stocks

Rules:

High single digit or double digit return on ROA, ROE, and ROCE

Long-term debt/OCF of less than 4

Debt to Equity of <50%, if above 50% then Long-term Debt/OCF 3 or below.

Stock holdings can be reduce to a min of 15 and max of 20.

Dividends will be received as cash and reinvested as opportunities present themselves.

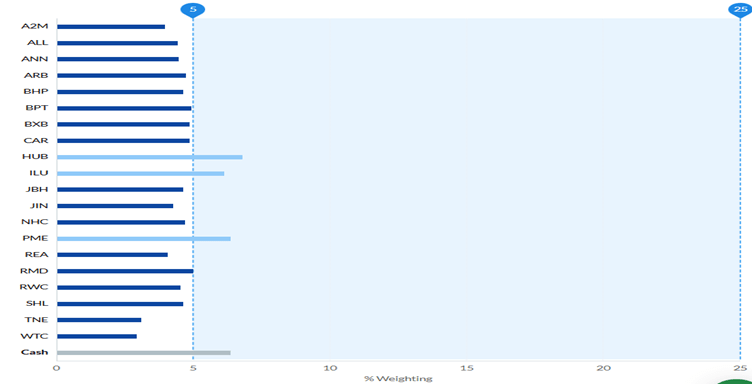

Individual Stock Weighting Limits:

Max weighting 25%

Min weighting 1%

No limit on cash% holding..

Performance

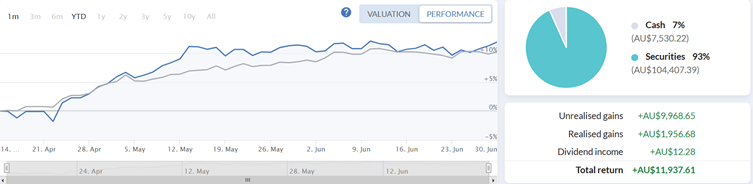

On 30th June the portfolio was up 11.94% Compared to the ASX All Ords which was up 10.22%.

The top 3 best performers for the quarter where TNE up 45.89%, PME up 37.61%, and HUB 35.66%. The bottom 3 worst performers where A2M -3.14%, JIN -1.90%, and ALL 0.14%.

Currently the portfolio is up 18.59% compared to the ASX All Ords which is up 13.16% since inception and the portfolio is worth $118,594 with a cash holding balance of $7,530, and is sitting on $18,594 of total returns since inception.

During the quarter Resmed (ASX: RMD) paid an interim dividend of 8.3c which equated to a $12.28 dividend payment to the portfolio, and is the first dividend received by the portfolio since its inception on 15th April 2025. Also, Telix Pharmaceuticals (ASX:TLX) and James Hardie (ASX:JHX) were removed from the portfolio. TLX was sold as it has to much debt and its ROA, ROE, and ROCE do not meet the investment criteria of the portfolio, see blow table.

JHX was sold on the back of their well-documented regulatory/governance issues on the back of their $8.75bn US acquisition of Azek.

The key issues are:

- Shareholder Dilution Without Vote: James Hardie received an ASX waiver allowing it to issue shares equal to 35% of its capital to fund the deal—without shareholder approval.

- Strategic Misalignment: Investors questioned the logic of acquiring Azek, which operates in a different segment (composite decking vs. fibre cement), and whether the premium paid was justified.

- NYSE Listing Shift: The move to the NYSE raised fears of weaker governance protections for Australian shareholders.

- Investor Backlash: Major funds like Australian Super and UniSupe publicly criticized the deal, prompting the ASX to launch a review of its listing rules.

On the back of these key issues the decision to sell JHX was made as it was poor form not to seek a shareholder vote and indicates to me that management is not aligned with shareholders.

ALL and ARB have replaced TLX and JHX in the portfolio as they meet the investment criteria and have been consistent performers of the years. You can read more on ALL here…

Also, TNE and WTC had their holdings in the portfolio reduced by half. This is an extract from the update regarding this on 21st June 2025, you can read the full update here…

Wisetech Global (ASX:WTC)

WTC currently has a PE ratio of circa 200, which is expensive and indicating a significant amount of future growth is already factored into its share price and investors are expecting substantial growth from WTC. WTC are up 30% since the portfolio inception in April this year.

Recently, WTC announced a $3.0bn strategic acquisition of the US based e2open, a company of similar financial size. e2open reported revenue of US$607.0 million and operating cash flow of US$111.4m, compared to WTC’s FY24 revenue of US$683.0m and operating cash flow of US$294.0m. Although both companies are similar in size, WTC is evidently more profitable as indicated by the significantly larger cash flow from operations. However, the acquisition raises questions about whether WTC can maintain its profitability while integrating e2open’s operations.

WTC’s investor presentation on June 26, 2025, emphasised that this acquisition is strategic rather than a bolt-on. A strategic acquisition aims to create value through synergies and cross/vertical integration over time, whereas a bolt-on acquisition would be EPS accretive from day one and immediately boost the bottom line. This long-term approach may not provide the immediate financial benefits expected by investors, and the integration process could be complex and risky, potentially impacting WTC’s financial performance.

As always with an acquisition the tell-tale sign will be the impact on ROE and ROA. As both these ratios should increase over the next 12-18 months due to the benefits of the acquisition, and the company is more profitable because of it. Time will tell.

Adding to the concerns, WTC has been experiencing turbulence at the board level, with two more non-executive directors announcing they will step down later this year. This instability at the top management level is troubling and adds weight to the decision to sell half of the portfolio’s WTC holdings. The uncertainty surrounding the company’s leadership and the challenges of integrating a major acquisition could negatively impact WTC’s future growth and profitability.

Technology One (ASX:TNE)

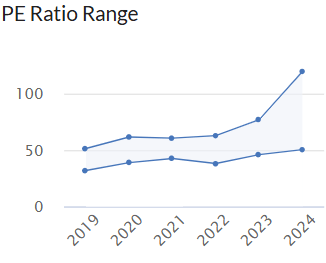

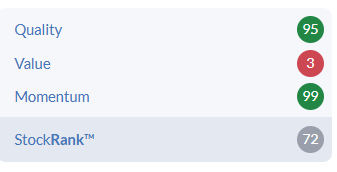

Since the inception of the portfolio back in April this year TNE is up 44% and is currently trading on a PE over 100 times earnings an on a forward PE of over 80 times. As can be seen in the graph below this is well above their previous PE range and for me is indicating the market has got carried away and it’s time to take some profits!

Furthermore, I will sell half of the portfolio’s Hub24 (ASX:HUB) holding as its valuations are beyond stretched and book some more profits in and increase the cash balance of the portfolio before reporting season and get ready to deploy some capital after the dust has settled post reporting season.

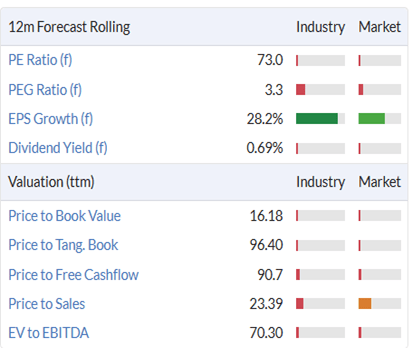

HUB Valuation Ratios. with a forward PE of 73 and Price to Free Cashflow of 90.7 are astronomical valuations and are the main reason I am happy to trim and take some profits.

Conclusion:

I am pleased with the performance of the portfolio and remain confident in its potential. The decisions made thus far have yielded positive results, and I am optimistic about the future. As we move forward, I will be closely monitoring the market for new opportunities that align with the investment criteria. By adhering to these established guidelines, I am confident the portfolio will continue to achieve its financial goals. I will be deploying capital as opportunities present themselves in the future and this is why I am happy to increase the cash balance now.

Disclaimer: Rational Share Investing With Ratios does not hold an AFSL and information on this site should not be considered financial advice, personal or general, and represents the views of the author.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of my holdings at a certain point in time, and the holdings may change over time.

Leave a reply to Portfolio Risk and Diversification – Rational Share Investing With Ratios Cancel reply